Last update: March 11, 2025

Cashew Market Report & Forecast

The project continues to make significant progress in providing stakeholders with reliable cashew market information. Timely updates on market trends, pricing, and supply chain dynamics have enabled informed decision-making. Our detailed monthly market report offers key insights and actionable recommendations, adding value to the cashew sector.

Current Cashew Price

- Export Prices: The average price per kilogram of raw cashew nuts in Guinea-Bissau currently ranges from 900 CFA Francs (US$1.50) to 1,200 CFA Francs (US$2.00). However, prices have fluctuated, occasionally dropping to 600 CFA Francs (US$1.00).

- Farmgate Prices: Farmers receive between 250 CFA Francs and 350 CFA Francs per kilogram, covering essential costs such as planting, pruning, harvesting, drying, and bagging.

February Market Forcast

As we move into February, several factors are expected to influence cashew prices:

- Harvest Season Impact: With harvesting activities increasing, a higher supply of raw cashew nuts may put slight downward pressure on prices. However, strong global demand could balance this effect.

- International Market Trends: Demand from major cashew-processing countries such as India and Vietnam is projected to remain strong, helping stabilize export prices.

- Exchange Rate Fluctuations: The CFA Franc’s performance against the US dollar may impact international pricing and export competitiveness.

- Local Market Conditions: If farmers and traders hold onto their stock in anticipation of better prices later in the season, this could lead to temporary supply constraints, potentially supporting farmgate price stability.

Regional Price Comparisons

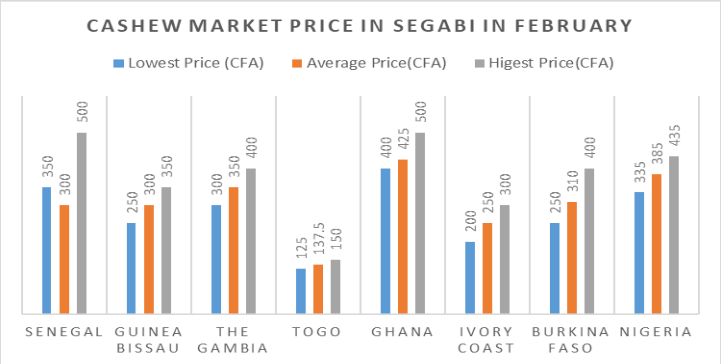

- In Senegal, raw cashew nut prices are comparable to Guinea-Bissau, ranging between 250 and 350 CFA Francs per kilogram. The retail price for processed cashew nuts in January was between US$7.59 and US$10.62 per kilogram (US$3.44 to US$4.82 per pound). Prices may fluctuate based on demand and supply conditions.

- In The Gambia, cashew prices are influenced by global market trends, nut quality, and consumer demand.

Overall, cashew prices in February are expected to remain within the 900–1,200 CFA Francs per kilogram range, with minor fluctuations depending on supply chain movements and global demand.

Staying informed about these market conditions will be crucial for all stakeholders in the cashew value chain. We will continue to provide weekly updates and detailed insights to help navigate these changes effectively.

Source: LIFFT Cashew Field Staff (Trade Pronotion & CMA Team)

Cooperatives provide information about how many tons of RCN is available in their storage. Please contact them directly using indicated phone numbers (WhatsApp).

Cooperative Name | Sales 2021 (T) | Sales 2022 (T) | Sales 2023 (T) | Sales 2024 (T) | Plan Sales 2025 (T) | Region | Tel/WhatsApp | Number of producers | Contact person | |

818 | 991 | 4,809 | 3,135 | 5,000 | Cacheu, Guinea Bissau | +245 96 662 81 14 | cooperativabuwendena@gmail.com | 650 | Antonio Preira Batista | |

14,932 | 33,323 | 7,001 | 2,931 | 8,000 | Cacheu,Guinea Bissau | +245 95 595 32 00 | mango_augusto@hotmail.com | 3 200 | Augusto MANGO | |

N/A | 1,486 | 37 | 2,995 | 3,000 | OIO, Guinea Bissau | +245 95 6105789 | cjammansaba2014@gmail.com | N/A | Malam Cani | |

1,203 | 2,224 | N/A | 1,789 | 3,000 | OIO, Guinea Bissau | +245 95 5369697 | cooperativaopro2020@gmail.com | 3 000 | Fatumata Camara | |

468 | 938 | 3,227 | 4,719 | 4,000 | Cacheu, Guinea Bissau | +245 95 555 36 66 | quecuto-augusto@hotmail.com | 600 | Papa Camara | |

N/A | 7,411 | 11,360 | 12,832 | 10,000 | Cacheu, Guinea Bissau | +245 95 6022413 | agrobigeni@gmail.com | N/A | Baciro Mane | |

1,292 | 651 | 670 | 3,153 | 3,000 | OIO, Guinea Bissau | +245 95 656 51 77 | wakilare2020@gmail.com | 1 000 | Mamadou Silla | |

1,945 | 4,362 | 16,502 | 10,963 | 12,000 | Cacheu, Guinea Bissau | +245 96 642 77 00 | cooperativalampadadecampo@gmail.com | 1 100 | Indjai Dabo | |

2,974 | 11,953 | 8,520 | 15,320 | 9,000 | Biombo, Guinea Bissau | +245 95 558 56 49 | ndelugan@hotmail.com | 800 | Daniel Ndjanaya Nanque | |

N/A | N/A | N/A | 3,199 | 3,000 | OIO, Guinea Bissau | +245 95 5265340 | casma@gmail.com | N/A | Baba Sighate | |

N/A | N/A | 9,626 | 16,604 | 9,000 | Biombo, Guinea Bissau | +245 95 5434869 | coop-ca@gmail.com | N/A | Moises Ca | |

N/A | N/A | N/A | 400 | 4,000 | OIO, Guinea Bissau | +245 95 5823849 | buwongktchif@gmail.com | N/A | Zacarias Quade | |

N/A | N/A | 220 | 220 | 2002 | Bafata Guinea Bissau | +245 95 570 26 60 | coopganadu@gmail.com | N/A | Braima BIAI | |

13 | 23,632 | 63,339 | 61,972 | 80,042 | 75,000 | 11 250 |

Cooperatives provide information about how many tons of RCN is available in their storage. Please contact them directly using indicated phone numbers (WhatsApp).

Cooperative Name | Sales 2021 (T) | Sales 2022 (T) | Sales 2023 (T) | Sales 2024 (T) | Plan Sales 2025 (T) | Region | Tel/WhatsApp | Number of producers | Contact person | |

1,108 | 1,622 | 1,722 | 3,393 | 2,500 | West Cost, The Gambia | +220 777 76 20 | kogies5212@yahoo.com | 1 500 | Kojo Mendy | |

N/A | 13 | 564 | 782 | 1,200 | North Bank, The Gambia | +220 386 86 08 | musanjsarr@gmail.com | 1 200 | Musa Sarr | |

191 | 32 | 420 | 469 | 700 | North Bank, The Gambia | +220 524 46 54 | musanjie139@gmail.com | 366 | Musa Njie | |

76 | 59 | 180 | 302 | 450 | West Cost, The Gambia | +220 248 85 75 | fonibintangc@gmail.com | 650 | Zakaria Gaye | |

128 | 79 | 39 | 52 | 150 | West District, The Gambia | +220 376 70 73 | aboudemba5@yahoo.com | 624 | Abou Demba | |

5 | 1,503 | 1,805 | 2,925 | 4,998 | 5,000 | 4,340 |

Cooperative Name | Sales 2021 (T) | Sales 2022 (T) | Sales 2023 (T) | Sales 2024 (T) | Plan Sales 2025 (T) | Region | Tel/WhatsApp | Number of producers | Contact person | |

1,311 | 3,179 | 4,679 | 1,708 | 3,000 | Goudomp, Senegal | +221 77 511 75 96 | fadegbagoudomp@gmail.com | 2 000 | Bacary Sonko | |

434 | 5,270 | 3,047 | 1,633 | 3,000 | Ziguinchor, Senegal | +221 77 410 11 59 | gieajac@gmail.com | 1 205 | Aliou Djiba | |

387 | 847 | N/A | 4,653 | 5,000 | Simbandi Balante, Senegal | +221 77 705 28 28 | nandomandina@yahoo.Fr | 1 155 | Valentin MANSALY | |

2,355 | 197 | 123 | 5,017 | 5,000 | Fatick, Senegal | +221 77 636 37 53 | amadoulaminecisse1960@gmail.com | 3 000 | Amadou Lamine Cisse | |

1,201 | 5,052 | 1,750 | 5,836 | 6,000 | Francounda, Senegal | +221 77 605 72 04 | laminecamara91@gmail.com | 1 000 | Younouss Mban Mansaly | |

775 | 261 | 128 | 998 | 1,850 | Kolda, Senegal | +221 78 198 65 38 | scoopcoumbacara@gmail.com | 630 | Youssouph Seydi | |

N/A | N/A | N/A | 453 | 650 | Ziguinchor, Senegal | +221 77 653 47 | bsdiatta@yahoo.fr | 356 | Tendouck | |

N/A | N/A | N/A | 265 | 500 | Sedhiou, Senegal | +221 792 71 26 | mc1560631@gmail.com | 145 | Manconomba | |

8 | 6,800 | 14,806 | 9,727 | 20,563 | 25,000 | 9,491 |

Visibility Support to Federations

The purpose of this support is to enhance the visibility and digital presence of agricultural federations in Senegal, The Gambia, and Guinea-Bissau by creating dedicated, user-friendly websites for each federation. These websites will serve as centralized platforms to showcase their missions, activities, and achievements, while providing valuable resources to members, partners, and the public. By highlighting success stories, promoting products and services, and facilitating better communication, the websites aim to strengthen the federations’ credibility, attract new opportunities, and foster collaboration. Ultimately, this initiative seeks to empower the federations to reach a wider audience, improve market access, and amplify their impact on local communities and the agricultural sector.

Senegal : EPTAS (Fédération des Producteurs et Transformateurs d’Anacarde du Sénéga).

Link: http://feptas.com/

The Gambia: The Federation of Gambia Cashew Farmers Association (FGCFA) is the national apex body representing all cashew farmers in The Gambia.

Link: https://www.fgcfa.com/

Guinea Bissau: FNCAPTC-GB(Federação Nacional das Cooperativas Agrícolas de Processadores Transformadores e de Comercialização da Guiné Bissau).

RCN collection information from 2020 to 2024 and collection forecasts in 2025

Sales 2020 (T) | Sales 2021 (T) | Sales 2022 (T) | Sales 2023 (T) | Sales 2024 (T) | Plan Sales 2025 (T) | Number of producers | Percentage of RCN Collected in FY25 | |

Total | 10,320 | 31,935 | 79,950 | 74,624 | 106,000 | 75,000 | 26,676 | 100% |

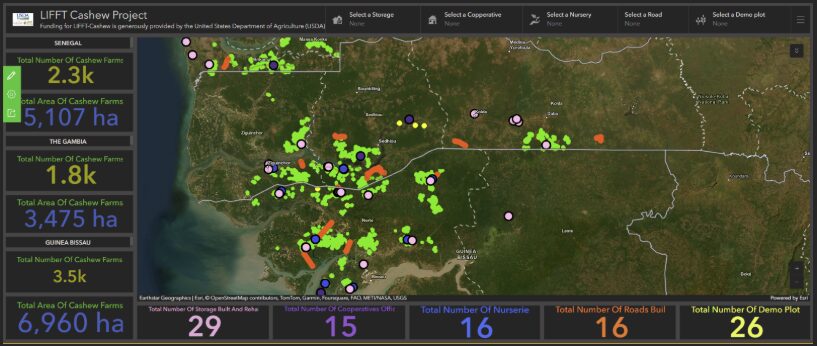

SeGaBi LIFFT Cashew Georeferencing

The link below offers a detailed visual representation of key assets and locations, including cashew fields, storage facilities, road networks, nurseries, cooperative offices, and demo plots. It enhances spatial analysis, supports informed decision-making, and provides stakeholders with an intuitive tool for monitoring and managing resources effectively.

The project highlights key statistics, such as the total number of cashew farms and the area they cover. Key points include:

Senegal 2.3k cashew farms mapped with an area of 5,107 hectares.

The Gambia has 1.8k cashew farms covering 3,475 hectares.

Guinea-Bissau has 3.5k cashew farms with 6,960 hectares.

The project has also led to significant infrastructure development, including the construction of storage facilities, offices, nurseries, roads, and demo plots. This initiative represents a substantial effort to support agricultural development and community opportunities in these regions. Further exploration of the project’s impact on local communities and the environment could provide deeper insights into its full benefits and challenges.